An unprepared audit can cost a nonprofit more than just time. It can cost credibility. Audit readiness turns that pressure into power by showing funders, boards, and communities that your organization runs on accountability, not anxiety.

1. Why Audit Readiness Matters

Audit readiness is more than financial housekeeping; it’s the backbone of trust. It proves your nonprofit can deliver clear, accurate, and compliant financial information whenever asked. When systems are well-structured and staff know their roles, audits become faster, cleaner, and less disruptive.

This guide shows how to prepare your documents, anticipate auditor expectations, and build everyday habits that make compliance second nature. It’s written for nonprofit leaders, finance heads, and community health organizations navigating federal audit requirements under the Electronic Code of Federal Regulations.

2. Trust, Transparency, and the Law: Why Audits Count

Funders expect clarity. They depend on financial statements and disclosures prepared under FASB ASC 958 to ensure funds are used responsibly. Transparent reporting builds trust and strengthens your reputation.

Audits also ensure you’re meeting legal standards. The Uniform Guidance outlines expectations for financial management and internal controls, while the Office of Management and Budget’s 2024 update raised the Single Audit threshold to one million dollars. The GAO’s Yellow Book reinforces independence and quality in government-related audits.

For nonprofit boards, solid audit preparation fulfills fiduciary duty and safeguards the organization from compliance risks and potential funding losses.

3. Inside the Auditor’s Lens

Auditors evaluate your nonprofit’s story through numbers. They use frameworks like FASB ASC 958 and ASU 2020-07 to assess how you classify assets and disclose in-kind donations. They rely on AICPA standards—AU-C 230 for documentation, AU-C 315 and SAS-145 for understanding risk, and AU-C 520 for analytical testing.

If you receive federal funds, Uniform Guidance Subparts D and F define the rules for financial management and audit compliance. The GAO’s Yellow Book adds another layer, emphasizing quality, ethics, and accountability in every audit engagement.

4. Your Audit Binder Blueprint

Preparation starts with organization. Create a digital audit binder with all your essentials: governing documents, board minutes, grant agreements, donor letters, in-kind valuation records, payroll reports, and reconciled bank statements.

- Governance & Policies: Founding documents, board minutes, and policy manuals proving oversight and internal control compliance under eCFR.

- Grants & Restricted Funds: Executed grant agreements, donor restrictions, and ledgers tied to the general ledger to meet Uniform Guidance §§200.302–200.303.

- Revenue & Receivables: Contribution details, in-kind valuation memos (ASU 2020-07), and receivable schedules for accuracy and disclosure.

- Disbursements & Procurement: Check registers, invoices, bids, and sole-source justifications aligning with federal procurement standards.

- Payroll & Timekeeping: Payroll registers, tax forms, and time-and-effort reports required for federally funded staff under the Compliance Supplement.

- Cash, Investments & Debt: Bank reconciliations, investment statements, and loan agreements with covenant evidence.

- Financial Statements & Close: Trial balance, lead sheets, variance analyses, and management’s closing checklist.

- Compliance & Other: Insurance, legal correspondence, tax forms, and SAM.gov/UEI documentation for federally funded entities.

Each document should trace directly to your general ledger. This transparency demonstrates that your financial systems meet the internal control requirements defined in 2 CFR 200.302 and 200.303. A clean binder saves hours when fieldwork begins.

5. File Like a Pro

An organized folder system is your hidden strength. Label folders by account number, use consistent date formats, and maintain a Prepared-By-Client index. Keep approved policies and meeting minutes locked.

Auditors look for clarity and consistency as much as content. Files should be complete, legible, and easy to follow from transaction to ledger. Under AU-C documentation standards, neat organization is the first sign of reliability.

6. The Pitfalls That Slow You Down

Every audit veteran knows the usual culprits.

- Missing approvals or written representations: Missing donor letters or grant approvals delay verification; centralize all approvals in a restricted-funds folder and require signoffs before closing.

- In-kind contribution misstatements: Incorrect valuation or disclosure of donated goods leads to findings; follow ASU 2020-07 and state categories and valuation methods clearly.

- Weak procurement documentation: Missing bids or justifications raise compliance issues; adopt a procurement policy under 2 CFR 200 and retain all quotes and approvals.

- Unreconciled balance sheet accounts: Unchecked accounts distort accuracy; reconcile monthly and use a close checklist with signoffs.

- Segregation-of-duties gaps: One person managing all steps increases risk; divide custody, recording, and approval duties, or add board/external review under AU-C 315 controls.

Avoid these setbacks by keeping all approvals in one place, following ASU 2020-07 for in-kind disclosures, and ensuring your procurement policy aligns with 2 CFR 200. Smaller teams can fill control gaps with board oversight or external accountant review, consistent with AU-C 315’s recommendations.

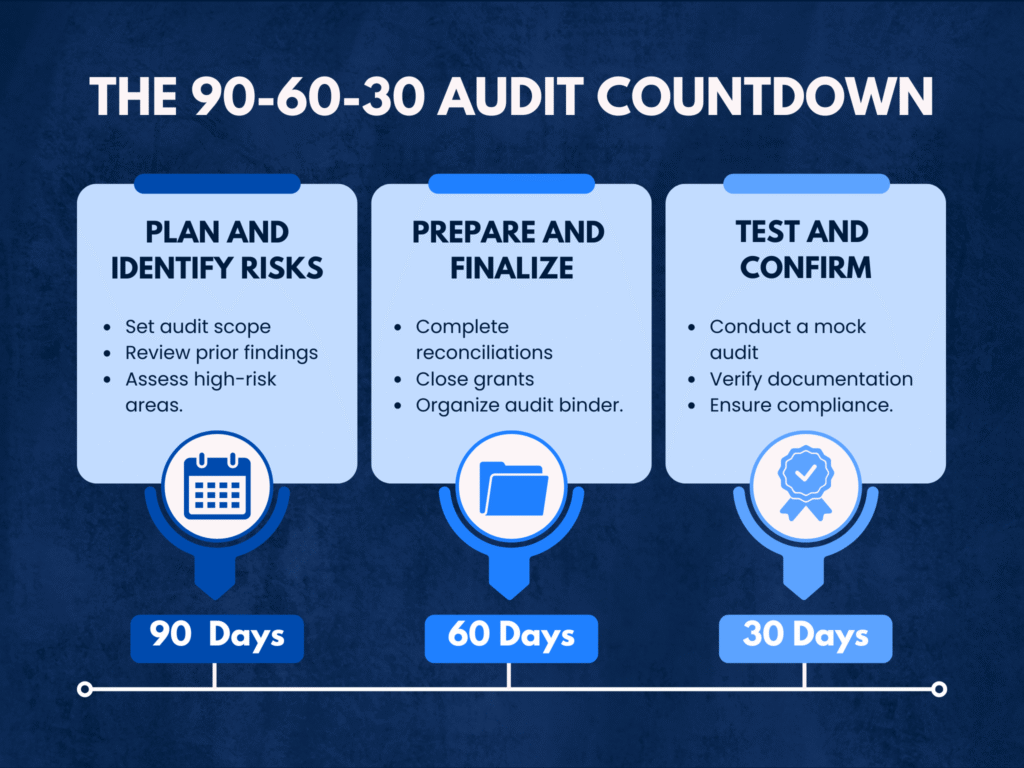

7. The 90-60-30 Rule

Think of your audit timeline in three phases.

- Ninety Days Before Fieldwork, focus on planning and risk. Confirm your audit scope, reporting framework, and federal awards to set clear expectations. Share prior-year findings, deliver a preliminary trial balance, and meet with your auditor to review high-risk areas such as restricted revenue and contributed assets.

- Sixty Days Before Fieldwork, concentrate on documentation. Complete all reconciliations and close your grant files with supporting reports and approvals. Prepare your audit binder, assign responsibilities for each file, and update compliance records and legal confirmations.

- Thirty Days Before Fieldwork, test your readiness. Conduct a short mock audit to ensure your team can retrieve records quickly and accurately. Finalize board minutes, confirm policy updates, and review Uniform Guidance documentation for procurement, subrecipients, and compliance reports.

A consistent 90-60-30 approach prevents last-minute rush and uncertainty. It allows your organization to approach the audit with structure, confidence, and professionalism. Readiness becomes routine, and the audit becomes a natural extension of your daily discipline.

8. Templates That Save You

Templates turn preparation into process. They save time, improve accuracy, and make complex audits easier to manage. When used consistently, they help your organization maintain audit readiness all year long.

- An Audit Prep Binder Index acts as your master tracker. It lists each request, its owner, location, and completion status, making coordination effortless. A clear index helps your team stay organized and allows auditors to find evidence without delays.

- A Monthly Close Checklist builds financial discipline. It outlines who performs reconciliations, reviews journal entries, and checks flux analysis each month. Regular use ensures that errors are caught early and documentation stays current and complete.

- The Restricted Funds Matrix tracks donor restrictions from award to release. It captures grant details, approval actions, and current balances, strengthening compliance under FASB ASC 958. When updated monthly, it prevents misclassifications and improves donor transparency.

- A Procurement Packet Cover Sheet summarizes every purchase. It records bids, methods, and approvals, aligning with federal procurement standards under 2 CFR Part 200. This small tool simplifies reviews and proves that your purchasing decisions meet policy requirements.

- The Segregation of Duties Map outlines who initiates, reviews, and approves key transactions. It helps detect gaps in oversight, especially in smaller teams with limited staff. Following AU-C 315 guidance, it documents controls that protect financial integrity.

- A Sampling Log supports internal reviews and mock audits. It lists the population, sampling method, selected items, and findings from each test. This record aligns with the auditor’s analytical approach and helps your team measure progress over time.

Together, these tools create consistency and accountability. They turn audit preparation from an annual scramble into a well-managed routine. Each one reinforces clarity, structure, and control, the hallmarks of a truly audit-ready organization.

Audit readiness should be an ongoing practice, not a seasonal task. Keeping financial management and internal control standards from 2 CFR 200 active throughout the year builds consistency and trust. Regular reviews of new FASB and GAO Yellow Book updates ensure your systems stay aligned with current expectations and avoid last-minute adjustments.

Treating each quarter as a light audit reinforces discipline and accountability. Reconciling accounts, updating restricted-fund schedules, and maintaining board approvals make readiness a daily habit. When staffing is limited, engaging an external accountant or CFO adds oversight that mirrors professional audit standards and strengthens long-term quality control.

For Federally Funded Nonprofits

Community Health Centers and other federally funded nonprofits need to monitor federal expenditures closely. Once spending reaches one million dollars, Single Audit requirements apply. Prepare time-and-effort certifications, procurement documentation, and subrecipient monitoring reports early. Aligning with the federal Compliance Supplement avoids costly findings later.

a. Restricted vs. Unrestricted: Getting It Right

Misclassification or delayed release of restricted funds remains one of the most common audit findings under FASB ASC 958. When contributions are recorded incorrectly, they distort the Statement of Activities and weaken donor confidence. Each contribution should be recorded at the time it is received, marked as either with or without donor restrictions, following ASC 958-605. Once a program or time condition is met, the related amount should be moved from “with donor restrictions” to “without donor restrictions” using a clear release schedule that links donor intent to program delivery.

Problems often arise when restrictions are released too early, delayed unnecessarily, or when restricted and unrestricted revenues are mixed in the general ledger. The simplest way to stay compliant is to assign each restricted grant its own sub-account or class and reconcile those balances monthly. This small step keeps your reporting transparent, your audit trail clear, and your credibility with funders intact.

b. Strength in Controls

Strong internal control over financial reporting (ICFR) builds confidence that your nonprofit’s numbers are accurate and trustworthy. It’s the foundation auditors rely on to assess how well your systems prevent errors, detect fraud, and ensure compliance with standards like AICPA AU-C 315 and SAS-145.

- Cash Receipts: Separate who handles, records, and reconciles incoming funds. This prevents one person from controlling the entire cash flow and reduces the risk of errors or fraud.

- Disbursements: Require dual approval for payments and include procurement review for large or unusual purchases. It ensures accountability and proper authorization before money leaves the organization.

- Financial Close: Have reconciliations and journal entries reviewed and signed off before closing each period. This confirms that balances are correct and all adjustments are transparent.

- Restricted Revenue: Keep a documented approval and release process for donor-restricted funds. It demonstrates that resources were used exactly as promised to funders.

- Limited Staff: If your team is small, introduce compensating controls such as monthly reviews by the board treasurer or an external accountant. Independent oversight strengthens credibility even without full segregation of duties.

c. The Letter That Speaks for You

Your management representation letter is your voice in the audit. It confirms that your books are complete, your disclosures accurate, and your management team accountable. Draft it at least a month before fieldwork begins. Doing so brings potential issues to light early and smooths the final review stage.

d. Guarding the Digital Frontline

Today, audit readiness extends beyond numbers. Auditors assess cybersecurity and digital file control as part of internal review. Use multi-factor authentication, assign user access by role, and keep secure backups. Define clear retention periods for audit evidence. Strong digital safeguards not only protect data but also prove compliance with modern Yellow Book standards for information integrity.

Audit readiness is no longer about surviving scrutiny. It’s about demonstrating trust. When a nonprofit treats accuracy, transparency, and digital responsibility as daily habits, an audit becomes less of a hurdle and more of a hallmark of good governance.

At Sheikh, Osher & Scott CPAs & Advisors, we help nonprofits move from reactive audits to year-round readiness. Our team builds tailored Audit Prep Binders, monthly close checklists, and restricted-funds matrices that match your unique funding streams. From organizing your records to walking through a mock audit, we guide your staff through a step-by-step thirty-day readiness sprint. The result is smoother fieldwork, faster turnarounds, and stronger confidence when it matters most.

Our goal is simple: to make your next audit proof of credibility, not chaos.